This is our first blog post as the new Connect Earth (aka our new Sustainable Finance OS), and we're glad you're here.

After bringing together the strengths of Connect Earth and Datia, we're stepping into this next chapter with one clear mission: to make sustainable finance simpler, clearer, and more actionable for everyone.

So when the draft for "SFDR 2.0" sent ripples through the sustainable finance world, we knew our first post had to be about this. SFDR is a major part of our client offering and the proposed overhaul is big enough that it deserves a grounded, calm explanation.

Let's break down what's going on, what might change, and how we're helping clients stay ahead without losing sleep.

Why SFDR Is Being Rewritten

The Commission has been clear: the original SFDR framework hasn't worked as intended.

Several challenges drove the need for reform:

- SFDR concepts became misaligned with other EU regulations like the EU Taxonomy and CSRD

- Financial market participants struggled to access reliable, complete ESG data

- Articles 8 and 9 were widely misused as quasi-labels, despite not being designed as such

- Disclosures ended up burdensome and not very helpful for end investors

Another important element of the proposal is the removal of portfolio managers and advisors from SFDR's scope, with their sustainability obligations instead addressed through MiFID II suitability rules. This is intended to reduce duplication between regulatory frameworks.

In short, SFDR needed a reset. And that's exactly what the Commission has proposed.

What's Actually in the SFDR 2.0 Proposal?

While the draft isn't final, the proposal gives us a strong sense of the direction.

1. Goodbye Article 8/9. Hello Three New Categories

The biggest headline is that the old Article 8 and 9 labels would disappear.

Instead, SFDR 2.0 introduces three new product categories:

- Transition: products supporting companies moving toward sustainability

- ESG / ESG Integration: funds that meaningfully consider sustainability factors

- Sustainable: products with explicit sustainability objectives at their core

The proposal also allows certain combinations of these categories, giving managers flexibility to reflect both transition and impact characteristics in a single product.

2. Clearer Standards (Including Thresholds & Mandatory Exclusions)

Each of the three categories comes with minimum investment requirements.

For example, at least 70% of a product's assets must align with the category's objective. This is one of the most significant changes and will prompt many managers to reassess their current product lineup.

In practice, category alignment could include investments in taxonomy-aligned activities, companies with credible transition plans or science-based targets, or portfolios referencing EU climate benchmarks.

The proposal also introduces mandatory exclusions, for example, around controversial weapons, certain fossil-fuel expansion activities, and violations of international norms. These are intended to create a more consistent baseline for sustainability-labelled products.

3. Simpler, Shorter Disclosures

Good news for anyone who's ever fought with the length of SFDR reports:

SFDR 2.0 proposes much more concise templates, with some just only two pages long. It's still compliance, but hopefully with fewer headaches. The goal is to make disclosures:

- Easier for investors to understand

- Less repetitive

- Less administratively burdensome

This is a shift for both investors and sustainability teams.

4. Removal of Key Concepts: Principal Adverse Impact (PAI) and "Sustainable Investment"

Two major structural changes:

- Entity-level PAI statements would be removed, reducing duplication with CSRD/ESRS. Some concept of PAIs on a product level may remain.

- The definition of "sustainable investment" (Article 2.17) will be removed completely as a concept and henceforth all disclosures relating to it will be removed as well, including the DNSH and Good Governance concepts.

5. Stricter Naming & Marketing Rules

If a fund isn't aligned with one of the sustainability categories, it likely won't be allowed to use sustainability-related terms in its name or promotional materials. This is meant to make sustainable finance marketing more honest and less noisy.

6. No Broad "Grace Period"

One of the surprising elements is the lack of a broad transition period.

What This Means for Asset Managers & Investors

Depending on your perspective, SFDR 2.0 is either:

- a much-needed simplification,

- or a serious shift that will trigger portfolio reviews, re-labeling, and strategic choices.

Realistically? It's both.

Here's the upside:

- Clearer product categories will help rebuild trust in sustainable investment claims.

- Investors will find it easier to compare products based on real, measurable criteria.

- Managers who genuinely invest sustainably will stand out more sharply.

Here's the downside:

- The removal of specific concepts can water down the definition of "sustainability"

- Certain frameworks like the Taxonomy may become less relevant

- Reduced transparency for end investors

Early reactions from across the market have been mixed. Many welcome the clearer structure and simpler disclosures and others are watching how the removal of concepts like DNSH can influence the practical meaning of "sustainability."

Where Connect Earth Comes In

Our rebrand comes at a moment when sustainability regulation is entering a new era of clarity, quality, and accountability.

We're here to help you:

- Understand what the new SFDR categories mean for your products

- Assess your current portfolios against the proposed criteria

- Identify gaps early before SFDR 2.0 becomes reality

- Build stronger, clearer sustainability reporting that investors actually understand

- Develop a future-proof fund strategy that aligns with both compliance and your sustainability ambition

We stay close to every regulatory update whether it is a proposal to draft to final legal text. All while translating it into practical guidance for your team.

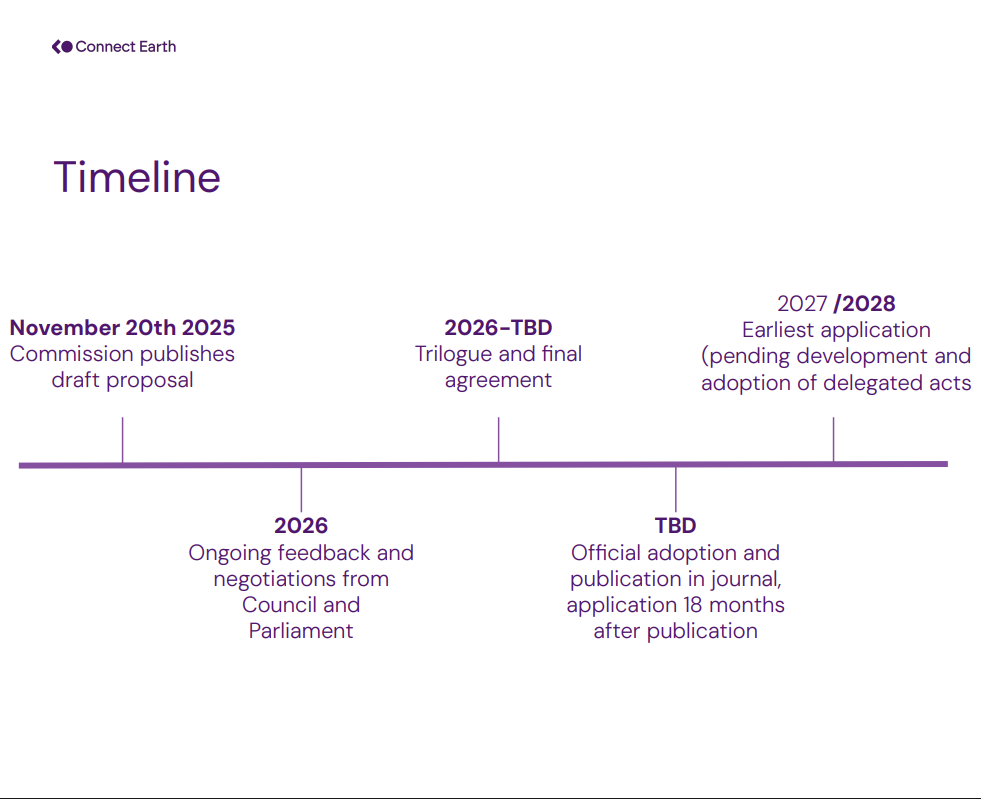

What Happens Next?

Even though the proposal reveals a lot, nothing is final until the European legislative process plays out.

We still expect:

- amendments to the proposal,

- detailed "Level 2" rules,

- and a clearer timeline for implementation.

But the direction of travel is unmistakable:

SFDR is moving toward clearer definitions, higher integrity, and simpler disclosures, and that's great to see for the entire market.

Let's Talk About Your SFDR Strategy

Whether you're managing existing Article 8/9 products, planning new ones, or simply curious about how SFDR 2.0 could reshape your sustainability approach, we'd be happy to walk you through what's coming.

Reach out now to our team and schedule a meeting!

Your sustainability strategy deserves clarity, and we're here to help you get there.